Page 381 - 2019 6th AFIS & ASMMA

P. 381

Lastly, let's compare with the factors across time. Before the 2009,

75-year-old borrower at seven percent interest rate environment can

borrow 60 percent of the house value. That amount decreased to

54.8percent immediately after the fund transfer to the MMI fund. So

that reflects the requirement to be self-sustained and not to lose money

or be subsidized. Then that factor keeps on dropping, and by today the

factor is only about 40 percent. So within the last ten years, there was a

20 points drop; it's a one-third decrease in the amount that the senior

citizen can receive from this reverse loan. So the question I want to put

here is whether this is desirable from the government's perspective.

Should the program be taking care of the senior and try to make them to

receive as much as they could on a fair basis? Or do we just need to make

sure that we don't tap into taxpayer dollars and charge the borrower for

those extra costs? Session III

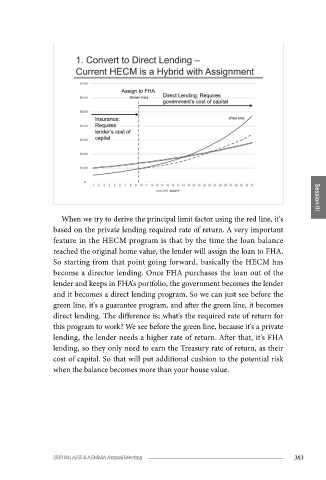

When we try to derive the principal limit factor using the red line, it's

based on the private lending required rate of return. A very important

feature in the HECM program is that by the time the loan balance

reached the original home value, the lender will assign the loan to FHA.

So starting from that point going forward, basically the HECM has

become a director lending. Once FHA purchases the loan out of the

lender and keeps in FHA's portfolio, the government becomes the lender

and it becomes a direct lending program. So we can just see before the

green line, it's a guarantee program, and after the green line, it becomes

direct lending. The difference is; what's the required rate of return for

this program to work? We see before the green line, because it's a private

lending, the lender needs a higher rate of return. After that, it's FHA

lending, so they only need to earn the Treasury rate of return, as their

Corresponding to that, the Congressional Budget Office, the US cost of capital. So that will put additional cushion to the potential risk

Congress, did research and by the end of last year, they published four when the balance becomes more than your house value.

different recommendations of how to change the HECM program. The

first one is to convert the program into a direct lending. That's exactly

what the audience asked in the second question earlier. So what's the

thinking behind that?

382 2019 6th AFIS & ASMMA Annual Meeting 383