Page 382 - 2019 6th AFIS & ASMMA

P. 382

Alternatively, if the government really wanted to make this a subsidy

program, they could also derive from the break-even point and extend

to the previous time. Anyway, since we have a lower cost of capital, we

can actually offer more loan amount to the borrower. So instead of 60%,

maybe you can raise it to 70%. So that is a policy decision; whether they

want to have the financial sustainability or to really subsidize these senior

citizens.

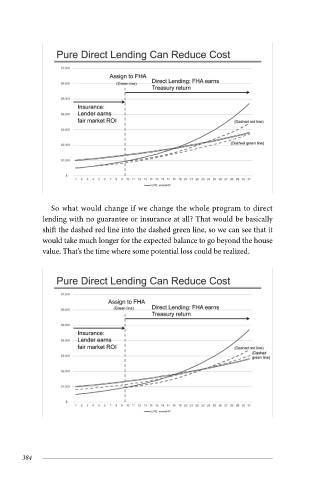

So what would change if we change the whole program to direct Session III

lending with no guarantee or insurance at all? That would be basically

shift the dashed red line into the dashed green line, so we can see that it

would take much longer for the expected balance to go beyond the house

value. That's the time where some potential loss could be realized.

Similarly, the second recommendation is to reduce the assignment

trigger level. So previously, the green line is the time the balance hits the

98% of the balance. If we reduce that trigger amount to a lower amount

to the pink line, then what will happen? We see that the loan balance

will hit that line at a much earlier date. So the effect is that it will actually

reduce the time period that the program requires the private rate of

return, basically reducing the overall cost of the program, and extending

the direct lending period while shrinking the insurance period.

384 2019 6th AFIS & ASMMA Annual Meeting 385